How to Analyse Financials for IPO Company (Retail-Friendly Guide)

Published on 24 Apr 2026, Friday

How to Analyse Financials for IPO Company (Retail-Friendly Guide)

Published on 24 Apr 2026, Friday

Why Financial Analysis Matters in IPOs When a company launches an IPO, you’re investing before market validation. Financial analysis helps you answer one key question: 👉 Is this business worth the price it is asking?

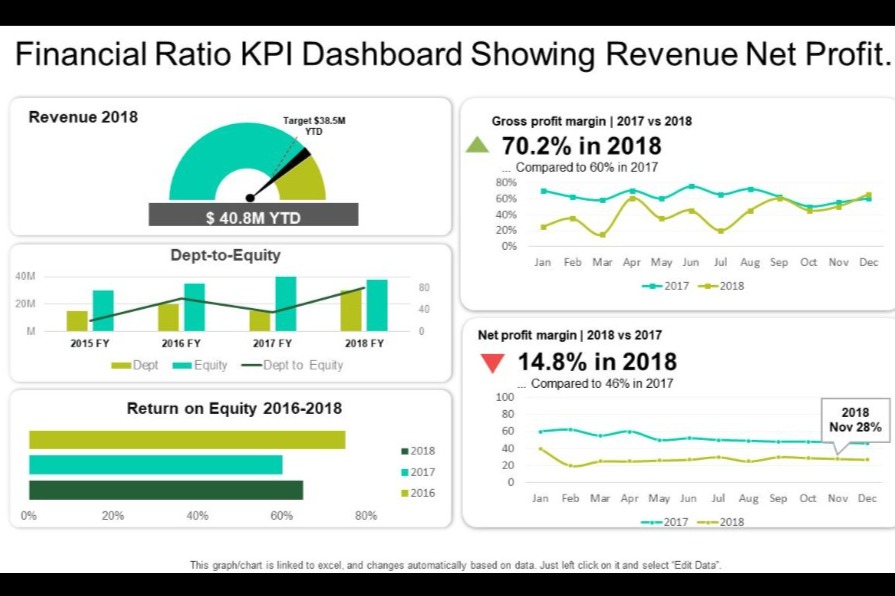

Step 1: Check Revenue Growth

Look at revenue for the last 3–5 years in the DRHP/RHP. What to check: Consistent growth (not sudden spike) Industry-aligned growth Avoid companies with flat or declining revenue Example Insight: Good: ₹500 Cr → ₹800 Cr → ₹1,200 Cr Risky: ₹500 Cr → ₹520 Cr → ₹1,500 Cr (sudden jump) 👉 Sudden growth may be temporary or manipulated through one-time contracts

Step 2: Profitability

Check: Net Profit EBITDA PAT margins Key Questions: Is the company profitable? Are margins improving? Healthy Sign: Profit growing faster than revenue Red Flag: Revenue rising but profit stagnant or falling

Step 3: Profit Margins

Focus on: EBITDA Margin Net Profit Margin Why it matters: Margins show efficiency + pricing power 👉 Compare with industry peers (very important) Simple Rule: Higher than peers = strong business Lower than peers = competitive pressure

Step 4: Debt Analysis

Check: Total Debt Debt-to-Equity Ratio Ideal Situation: Low or reducing debt Red Flag: High debt + IPO money used to repay loans 👉 This means IPO is not for growth, but for survival.

Step 5: Cash Flow

Check: Operating Cash Flow (OCF) Golden Rule: 👉 Profit without cash flow = danger Good Sign: Positive and growing cash flow Bad Sign: Profit positive but cash flow negative

Step 6: Return Ratios

Focus on: ROE (Return on Equity) ROCE (Return on Capital Employed) Ideal Benchmark: ROE > 15% ROCE > 15% 👉 Higher ratios = efficient management

Step 7: Valuation

Check: P/E Ratio Price to Sales (P/S) Compare with: Listed peers Decision Logic: Overpriced IPO = Avoid / Caution Fairly priced = Consider Undervalued = Opportunity

Step 8: Use of IPO Funds

Read this section carefully in DRHP. Good Use: Expansion New projects Debt reduction (partially) Bad Use: Only debt repayment Promoter exit (OFS heavy)

Step 9: Key Red Flags

Watch out for: Sudden profit jump before IPO High receivables (money not collected) Negative cash flow Promoters reducing stake heavily Frequent related party transactions

Final IPO Financial Checklist

Before applying, ask: ✔ Is revenue growing steadily? ✔ Is the company profitable? ✔ Are margins strong vs peers? ✔ Is debt under control? ✔ Is cash flow positive? ✔ Are returns (ROE/ROCE) good? ✔ Is valuation reasonable? 👉 If most answers are YES → Strong IPO candidate 👉 If many NO → Avoid or high risk Most retail investors only see GMP or subscription numbers. 👉 But smart investors combine: Financial strength QIB subscription Valuation This gives a complete IPO picture

Disclaimer

This content is for educational purposes only. We are not SEBI-registered advisors. IPO investments are subject to market risks, including potential loss of capital. Always do your own research before investing.

Key Financial Terms Explained (IPO Analysis Made Simple)

Net Profit

What it means: Final profit after all expenses, tax, interest. Formula (simple): Revenue – All Expenses = Net Profit How to analyse: Growing = good sign Declining = warning 👉 This is the real earning of the company

EBITDA

Full Form: Earnings Before Interest, Tax, Depreciation & Amortisation What it means: Profit from core business (ignores financing & accounting effects) Why important: Shows operational strength Useful for comparing companies 👉 High EBITDA = strong business operations

PAT Margin (Profit After Tax Margin)

Formula: PAT Margin = Net Profit / Revenue × 100 What it means: How much profit company earns from ₹100 sales Example: 10% margin = ₹10 profit per ₹100 revenue 👉 Higher margin = better efficiency

Total Debt

What it means: Total loans taken by company How to analyse: High debt = risky Low debt = safer 👉 Always check if IPO money is used to repay debt

Debt-to-Equity Ratio

Formula: Debt/Equity = Total Debt / Shareholder Equity What it means: How much company depends on borrowed money Ideal: < 1 = safe 2 = risky 👉 High ratio = financial pressure

Operating Cash Flow

What it means: Actual cash generated from business Important Rule: 👉 Profit is accounting, cash is reality Good Sign: Positive & growing OCF Bad Sign: Profit high but cash flow negative

ROE (Return on Equity)

Formula: ROE = Net Profit / Shareholder Equity × 100 What it means: How efficiently company uses investors’ money Ideal: 15% = strong 👉 Higher ROE = better management efficiency

ROCE (Return on Capital Employed)

Formula: ROCE = EBIT / Total Capital × 100 What it means: Return generated from total capital (equity + debt) Why important: Better than ROE when company has debt 👉 High ROCE = efficient use of capital

P/E Ratio (Price to Earnings)

Formula: P/E = Share Price / Earning Per Share What it means: How much investors are paying for ₹1 earnings Example: P/E = 20 → paying ₹20 for ₹1 profit How to analyse: Compare with peers High P/E = expensive Low P/E = cheap (or weak business)

Price to Sales (P/S Ratio)

Formula: P/S = Market Value / Revenue What it means: How much investors are paying for ₹1 sales When useful: Loss-making companies Early-stage companies 👉 Lower P/S is generally better

| Metric | What It Tells | | ----------- | ------------------- | | Net Profit | Final earning | | EBITDA | Business strength | | PAT Margin | Profit efficiency | | Debt | Financial risk | | Debt/Equity | Leverage level | | OCF | Real cash | | ROE | Return to investors | | ROCE | Capital efficiency | | P/E | Valuation vs profit | | P/S | Valuation vs sales |

Pro Tip (Important for IPORupee Users)

Most people: 👉 Only see GMP + Subscription Smart analysis: 👉 Combine Financials (above metrics) QIB subscription Valuation This is where your platform can dominate if you simplify this visually.

Disclaimer

This content is for educational purposes only. We are not SEBI-registered advisors. IPO investments are subject to market risks, including potential loss of capital.